While financial advisors may tell their clients to think of their life in financial buckets, it’s not exactly the easiest framework to focus on. Whether it’s because the concept seems too abstract or that people can only easily focus on the present, compartmentalizing finances is tricky at best.

One of the reasons thinking in financial buckets can seem like a pipe dream is that people who are particularly stressed or pushed to their max have a difficult time focusing on anything other than the present. Sure it makes sense for a 30-year-old to be planning for their retirement, but if that person could be using those savings for the down payment on a house, it’s challenging not to allocate funding to the present or near future.

Add to that anyone’s personal history and/or traumas related to money – whether that’s feelings of shame, guilt, inability to manage properly, etc. – and you’ve got a recipe for complacency.

Tips to Start Bucketing

The purpose of a bucket system is to start dividing money mentally – allocating it to where it ought to be used so there aren’t funds metaphorically screaming to be spent.

Whether it’s compartmentalizing related to life stages such as retirement or whether it’s having a bucket for fun times and other buckets allocated for specific purchases, this practice can help you achieve your financial goals without destroying other opportunities or areas of your lives.

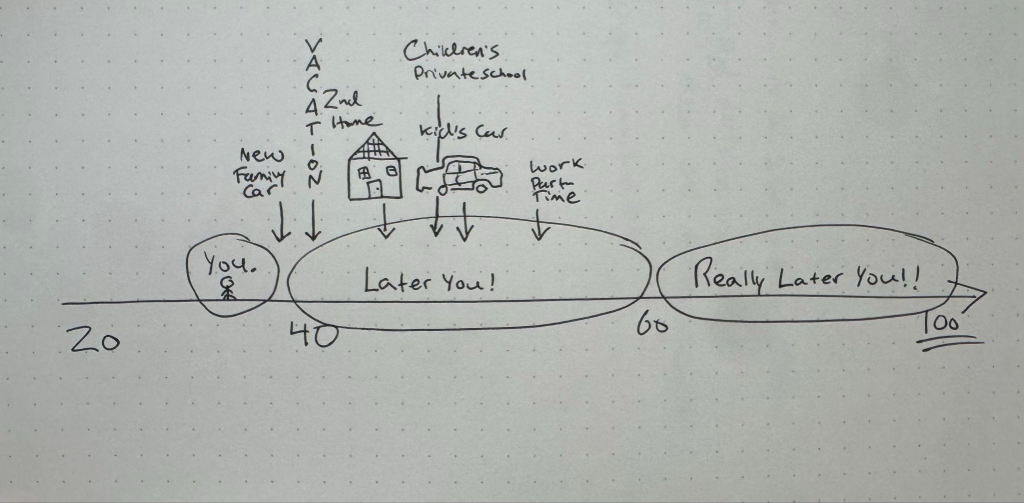

Give every dollar you earn a “Bearing and a Bingo.” The bearing is where that dollar is headed; next family car, kid’s wedding, or funding a sabbatical in 7 years. “Bingo Fuel” is pilot-speak for the minimum fuel required to return to base or ship (especially, if the ship is sailing in the other direction). With your money, Bingo is your deadline when that dollar needs to be used.

Another way to look at it is giving every dollar a job. For example, the first dollar you make could be allocated to your mortgage, the second could be to pay student loans, and the third is to be saved toward a child’s education. This helps to avoid overspending, increase investment contributions and makes it easier to understand where your money is going.

The first step in following this process is determining your “why.” Once that has been established, it’s much easier to follow a new set of protocols because the purpose is understood. Next, come up with a list of outcomes for your present and your future. Then, automatically allocate to those goals from your current income. From there, sit back and anticipate how future you will appreciate what present you is doing.

Another way to make this process easier is to literally separate the money based on its assigned purpose. That could mean having a brokerage account and a bank account or having several bank accounts that are each labeled based on their purpose.

And give yourself grace when things aren’t perfect, as no one is. Certainly there are times when we borrow from tomorrow for today. We do it with our sleep and health too, but every step toward this compartmentalized state is another one toward the financial life you want to achieve.

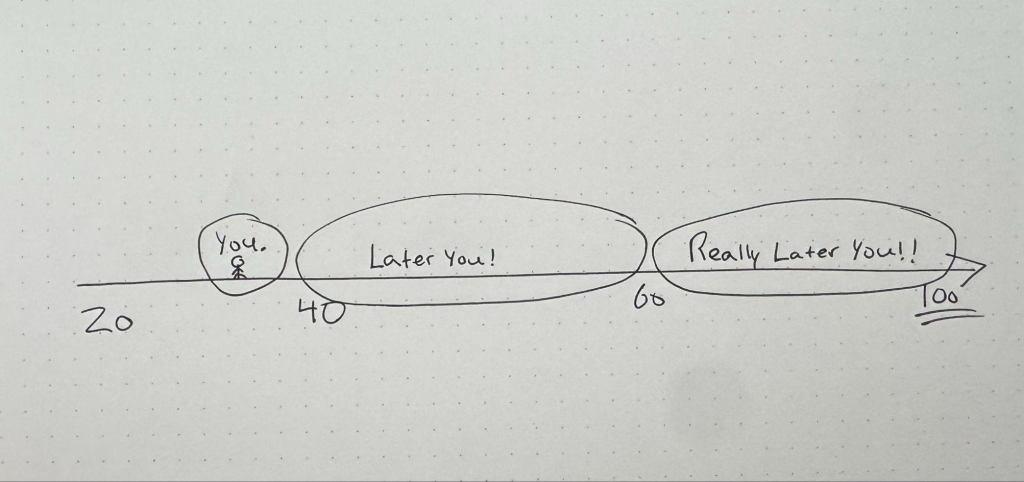

I would also encourage you to select the bare minimum number of buckets at first. The easiest three for me to visualize have to do with time – that is now, age 60+ (Since most retirement accounts have tax benefits there) and then the middle.

Certainly it’s challenging to go from one central financial pot to a dozen small buckets. But amping up from one to two or three and then gradually adding one as is appropriate or desired is much easier.

Sometimes even the name of the bucket can make that savings or goal feel more tangible and doable. For instance, labeling a bucket for travel associates your love of new destinations or the feeling of vacation with this bucket. Who wouldn’t want to add more money in there to make that goal achievable?! Particularly if you’re doing more boring tasks with your money like paying off debt, pairing it with something fun or a reward of some kind helps with adherence.

Thrivent and others have shown that the bucket approach can help investors manage against market risk in the short-term while still increasing their longer-term holdings.

Find a manageable path for yourself or work with a financial advisor to determine the best strategy for you. Advisors can be that empathetic ear that will help you understand your true priorities and goals while also lending their financial expertise in determining how to achieve those.