What is Direct Indexing

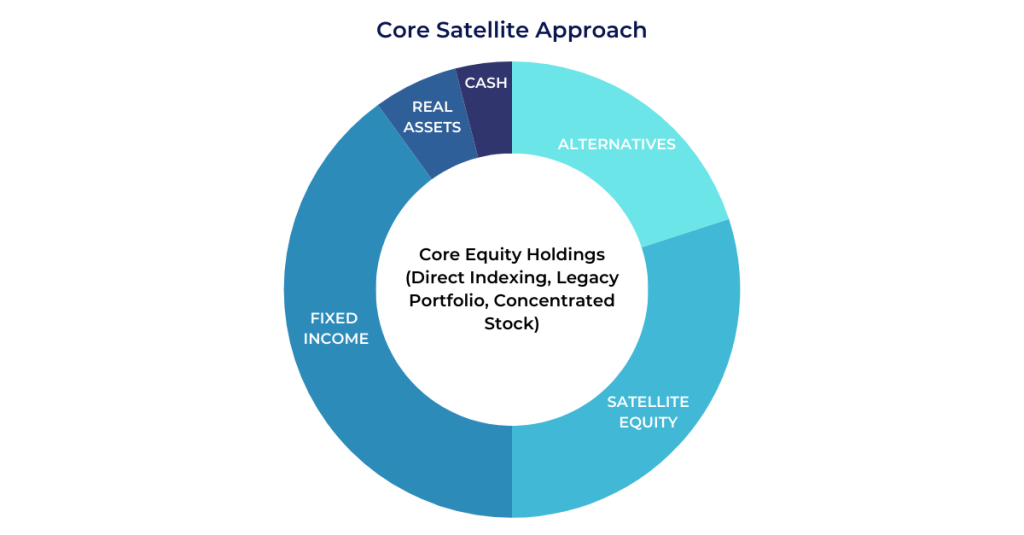

For many investors, a core equity strategy is the centerpiece of a diversified investment portfolio, and this core is often represented by indexed exposure to core equities with “satellites” representing other asset classes completing the overall asset allocation.

Direct Indexing strategies, which provide investors the ability to calibrate their core equity exposure to an index by directly owning the individual component stocks, have proliferated in recent years.

Their appeal is straightforward: like index funds, these strategies can provide performance generally in line with the market, but rather than owning shares in a commingled vehicle such as an ETF or mutual fund, investors own a selection of the individual securities that make up the index in a separately managed account (SMA).

An investor who obtains their core equity exposure and market performance through a direct indexing portfolio can often benefit from some key additional attributes, such as:

- portfolio customization to align with individual needs and preferences, such as social, environmental, or personal values

- reducing exposure to a particular stock or sector where the investor may have concentrated risk elsewhere in their portfolio, or their profession

- tax loss harvesting, which can enable an investor to potentially enhance after tax returns by strategically realizing capital losses throughout the year.

Tax Loss Harvesting

Tax loss harvesting involves selling a stock or other assets at a loss and using that realized loss to offset realized capital gains from other investments. These could be alternative investments, such as hedge funds or private equity, a concentrated stock position, or even the sale of a home or business. Whatever the source of capital gains, tax loss harvesting may allow the investor to offset some of these gains and generate tax savings.

Direct indexing portfolios generally offer greater opportunities to harvest capital losses versus portfolios of ETFs or mutual funds because at any point in time, not just at year end, any individual name and tax lot held in the direct indexing portfolio may represent a loss harvesting opportunity. Investors in a broad market ETF or mutual fund, by contrast, can only realize capital losses by selling their position when the entire position (market) is down.

Portfolio Ossification

But what happens when there are no losses to harvest? You’ve done everything right. Now what?

Many investors who have wisely deployed direct indexing or other investment strategies and benefited from the strong market performance of the last 2 or even 20 years now find themselves with new challenges: their portfolios are overweighted with risk assets, over concentrated in a handful of high performing stocks, or they simply have no strategy at all anymore, unable to de risk or rebalance due to excessive capital gains tax liability. In any case, we call this portfolio “ossification”, or “capital gains paralysis” and the dilemma, unresolved, carries risks of its own.

Some Solutions to Consider

Fortunately, there is no shortage of solutions to consider for the “nice problem to have” of portfolio ossification. Here we highlight just a few.

- 1. Deploy a new Managed Account strategy: Overlay the core equity portfolio with an options based or long short strategy to rejuvenate loss harvesting, restore balance, and continue to add tax alpha (discussed further below)

- 2. Fund Philanthropic Goals: Donate appreciated shares, perhaps utilizing a Donor Advised Fund (DAF), Charitable Remainder Trust (CRT), or Charitable Lead Trust (CLT) to receive a charitable deduction, minimize capital gains taxes, and create an income stream or legacy gift

- 3. Exchange Fund: Investors with low cost basis positions, high tax rates, and minimal liquidity constraints may consider using an exchange fund to achieve diversification without triggering immediate tax consequences

- 4. Gift Shares to Family: This strategy can reduce the size of the concentrated position and shift future appreciation to family members. Gifting stock can also help with estate planning by reducing the size of the taxable estate

- 5. Acceptance: Recognize the tax cost as an unavoidable consequence of successful investing, diversify gradually , designating a fixed capital gains tax budget each year, and maintain rebalancing discipline within set parameters. By spreading out the sales and reinvesting the proceeds into a diversified portfolio over time, investors can manage the tax impact more effectively and reduce the risk of timing the market poorly

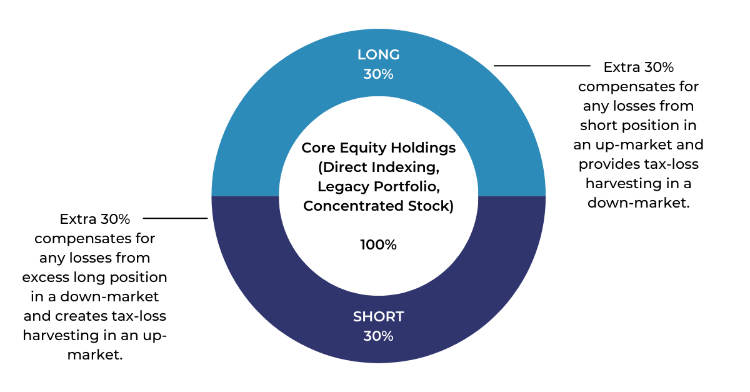

A closer look at Option #1, the “130/30”

An increasingly accessible tax loss harvesting strategy for an ossified portfolio is one that can generate tax benefits in both rising and falling market environments and for periods much longer than traditional long only tax loss harvesting. An example of such a strategy is the 130/30. This next evolution of tax loss harvesting starts with a portfolio of equities benchmarked to the index of the client’s choice but then overlays additional long positions equivalent to 30% of the account value, along with 30% short, for 130/30 in total. The specific parameters are client specific, flexible and customizable.

Merits of a long short approach

In such a structure, the short positions in the portfolio serve an important purpose. As the market rises, the 30% short side of the extension will likely have positions that have lost value, potentially leading to candidates on the short side to generate tax losses. Conversely, in a year where equity markets fall, the 130% long side of the extension will likely have positions that have fallen in value, potentially leading to candidates on the long side to generate tax losses. Meanwhile, the core portfolio can continue to perform in line with the targeted index. With this long short approach, the ability to generate tax losses is present regardless of market conditions and even if the original core portfolio has been in place for years and is highly appreciated.

Key Benefits

The value of a strategy with a long short extension may not be limited to the tax benefit it provides but may also include the consistency and flexibility of that benefit. The tax benefits of a traditional tax loss harvesting strategy, on the other hand, can be sporadic, only during market declines, or only available in early years of a strategy, and therefore less valuable as a planning tool. A long short extension may also be a helpful tool for managing account risk (tracking error) versus a stated equity benchmark, along with generating a tax adjusted return in addition to the underlying equity benchmark, or even to generate losses that can be used to offset gains outside of the portfolio.

Conclusion

The purpose here is not to advocate for any particular investment strategy or solution. Tax optimization in the context discussed here can be complex and requires a full understanding of the mechanics, costs and risks. The conclusion is, however, that if any of the following are true…

- Your portfolio is “ossified” as discussed herein

- You are concerned about the level of risk or concentration in your portfolio but feel paralyzed based on an aversion to incurring capital gains taxes

- You are concerned about an upcoming significant capital gain (from the sale of a business or real estate transaction, for example) and seek potential losses to offset

…there may be compelling solutions that you can thoughtfully consider in consultation with your financial and tax advisors rather than simply accept that you are “stuck” and have no choices at all.