Which Is Better for Education and Long-Term Wealth?

The IRS recently issued formal guidance on many, though not all, of the rules governing Trump accounts. That has prompted financial planners to ask where this new tool fits in the broader ecosystem of tax-advantaged savings vehicles. A key question is how Trump accounts, also known as “530 A” or “American Dream” accounts, stack up against 529 Plans, formally called qualified tuition programs. This article highlights when one, the other, or a combination may make the most sense.

Basics of Trump Accounts and 529 Plans

Trump accounts were inspired by hedge fund manager Brad Gerstner’s, “Invest America” idea, which proposed government funded accounts at birth that could be accessed only in adulthood for education or entrepreneurship as a way to address multigenerational poverty. Under the current pilot program, in effect from 2025 through 2028, the federal government will contribute $1,000 for each eligible child when a Trump account is opened during that window.

Beyond this seed money, total additional contributions of up to $5,000 per year can be made until the child turns 18. Trump accounts may also be opened for older children up to age 18, though those accounts do not qualify for the $1,000 deposit. Contributions can come from family members, other individuals, and corporations, and must be invested in ultra-low-cost stock market index funds.

No distributions are allowed before the calendar year in which the beneficiary turns 18. Starting in that year, the account can be used for qualifying expenses such as education, a first-time home purchase, or starting a business. Withdrawals are taxable on a pro rata basis between contributions and earnings but avoid the 10 percent early distribution penalty if used for those qualified purposes. Alternatively, the assets can be left invested for retirement or converted to a Roth IRA, where future growth can be tax free if Roth rules are followed.

529 plans, in contrast, were created in 1996 to promote saving for education. They allow after tax contributions to state-sponsored investment programs. Earnings and withdrawals are tax-free at the federal level when used for qualified education expenses, which now include higher education, certain trade schools and certifications, and, within limits, K-12 private tuition. While individual 529 plans have lifetime contribution caps, often around $300,000, there is effectively no overall limit because multiple 529 accounts can be opened for the same child.

529s are also highly flexible. Owners can change the beneficiary from one child to another, apply unused balances to future grandchildren, or even name themselves as the beneficiary. Non-qualified withdrawals are taxable and subject to a 10 percent penalty on the earnings portion. Recent law changes also allow up to $35,000 dollars of leftover 529 assets to be rolled to a beneficiary’s Roth IRA over time, subject to a 15 year seasoning period and annual Roth contribution limits.

Education Funding: 529 Plans Usually Trump the Trump Account

For families whose primary objective is funding education, especially college and possibly K-12 private school, 529 plans generally come out ahead. They allow larger long-term contributions, provide access to diversified investment options, and offer fully tax-free withdrawals for qualified education expenses, including certain K 12 costs.

However, Trump accounts can still play a valuable role, particularly for lower income families that might never set up a 529. The automatic $1,000 contribution for children born during the pilot years creates a modest but meaningful starting balance even when parents cannot contribute much. If family income remains low, the tax cost of using the account or converting it to a Roth IRA may be nominal.

However, for moderate to high income families, Trump accounts have a key drawback when used for education. Taxable education distributions may be subject to the kiddie tax rules, which apply the parents’ top marginal rate to a child’s unearned income above a threshold. At present, there is no exception for Trump account withdrawals used for education. That may further reduce the Trump account value relative to 529 plans, where qualified withdrawals are tax-free.

One unique feature of Trump accounts is the ability for employers to contribute up to 2,500 dollars per employee per year. Those contributions are deductible to the company, not subject to payroll tax, and currently not taxable to the employee. There is no comparable employer contribution framework for 529 plans. For workers whose employers participate, this benefit can make Trump accounts a valuable complement to 529 savings.

Retirement Savings: Trump Accounts Shine

For retirement planning, Trump accounts may be the more powerful tool. Taxpayers hav have long pined for a tax-favored way to begin saving for children’s retirement beginning from birth, but the earned income requirement for traditional and Roth IRAs has made that nearly impossible for young children. Trump accounts bypass that hurdle by allowing contributions from birth with no earned income requirement.

At age 18, beneficiaries can roll Trump account balances into traditional IRAs or convert them to Roth IRAs. Accurate recordkeeping is essential to ensure that after tax contributions are not taxed again upon withdrawal. Any income tax due on a Roth conversion should ideally be paid from outside funds, since using account assets to pay tax can trigger a 10 percent early distribution penalty and reduce the long-term benefit.

One potential strategy that has been largely overlooked to-date is to roll the Trump account into a traditional IRA at 18 and then execute partial Roth conversions over several low income years. This approach can allow beneficiaries to migrate most or all of the balance into a Roth IRA at relatively low tax cost. With steady contributions from parents and employers, it is realistic for some Trump accounts to reach $200,000 or more by age 18, giving young adults a substantial head start on retirement.

By comparison, 529 plans offer only limited retirement utility. The ability to roll up to 35,000 dollars to a Roth IRA is helpful for leftover funds but does not transform 529s into primary retirement vehicles.

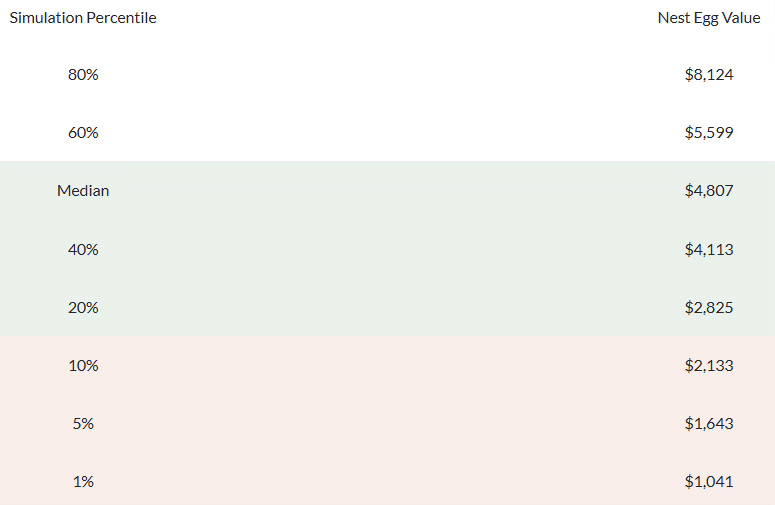

Projected Value of a $1,000 Trump Account after 17 Years Assuming No Future

Contributions and a 100% Allocation to an S&P 500 Index Fund with an .05% expense ratio:

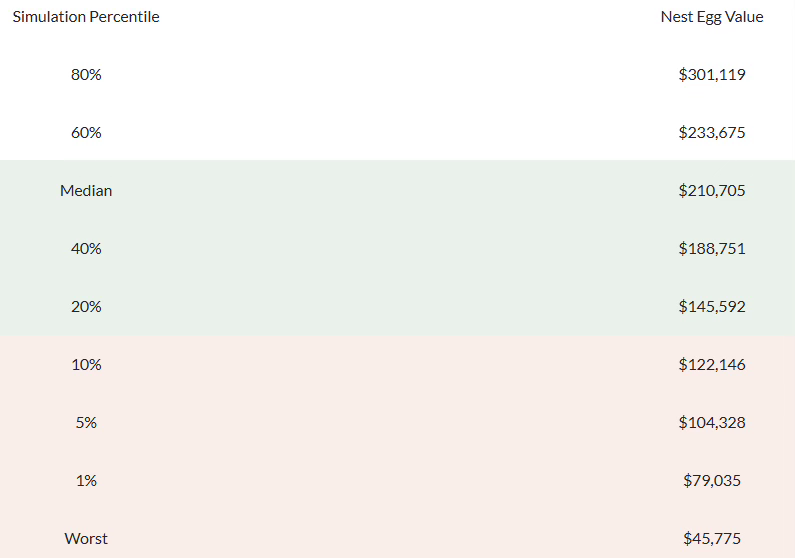

Projected Value of a Trump Account after 17 Years Assuming Maximum $5,000 Annual Contributions and a 100% Allocation to an S&P 500 Index Fund with an .05% expense ratio:

Other Uses and Overall Verdict

For goals beyond college and retirement, the two account types diverge again. Trump accounts allow qualified distributions for a first-time home purchase and for funding a business without the 10 percent penalty, though earnings remain taxable. That makes them appealing for families who may want to preserve options for home ownership or entrepreneurship.

529 plans, on the other hand, are better suited for consumers who value K-12 private schooling and multigenerational planning. They allow tax free withdrawals for certain K-12 expenses. which Trump accounts do not permit distributions before the year the beneficiary turns 18. 529 plans’ flexibility to change beneficiaries and support future grandchildren also makes them a superior multigenerational education tool.

In my view, nearly every family with a child born during the pilot should capture the $1,000 Trump account incentive. For ongoing education savings, 529 plans will remain the primary vehicle for most middle and higher income families, while Trump accounts serve as a complement, particularly when employer contributions are available. For families whose main objective is to give a child a powerful headstart on retirement, Trump accounts seem like the clear winner.

Crucially, this is not an either or decision. Many families will be best served by opening both: a Trump account to capture the government funding, employer contributions, and preserve the option for long-term retirement or entrepreneurial applications, and a 529 plan to serve as the main engine for education funding. Used together, they can support education, home ownership, business creation, and retirement security in a way that neither can fully achieve alone.

Trump account may be established beginning July 4, 2026 by submitting IRS Form 4547. The entire enrollment process is provided at TrumpAccounts.gov.

John H. Robinson is the owner/founder of Financial Planning Hawaii and

Fee-Only Planning Hawaii.