When investors choose a financial advisor, they often focus on investment performance, fees, brand recognition, or the size of the firm. Those factors matter. But I would argue there is a more important question underneath all of them.

When there is tension between what is best for the client and what is best for the institution, who ultimately comes first?

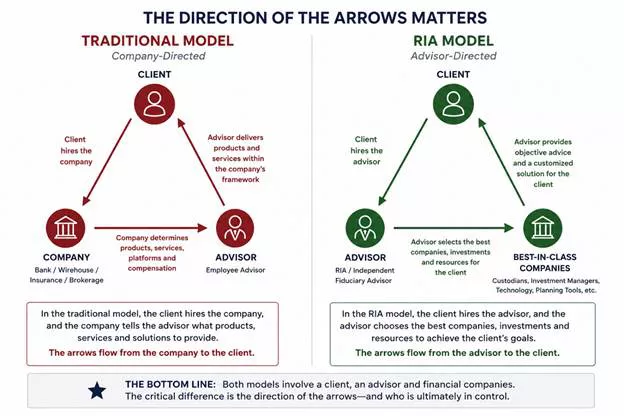

One of the simplest ways to think about wealth management is through the image of a triangle. At the top sits the client. At the two bottom corners are the advisor and the financial firm. The critical issue is not whether all three parties are involved; they almost always are. The critical issue is the direction of the arrows.

The traditional wirehouse, bank, insurance, and brokerage models are generally built around the first version of the triangle. The client hires a large institution, and the advisor operates within that company’s framework. To be clear, this does not mean the advisor is bad or unethical. Many employee advisors are talented, hardworking professionals who genuinely care about their clients. Large firms can also provide significant resources, recognizable brands, and sophisticated infrastructure.

However, the advisor is ultimately operating within a corporate ecosystem. Investment platforms, approved products, compensation structures, technology, and service models are often determined from the top down. Even when an advisor strives to be objective, they are working within boundaries established by the institution. The institution may not dictate every recommendation, but it does shape the menu of available choices. In that sense, the arrows primarily flow from the company to the advisor and then to the client.

The Registered Investment Advisor, or RIA, model was largely built to reverse those arrows. Importantly, I am not referring to every form of “independence” in wealth management. Some independent broker-dealer models still retain many of the same platform limitations and product-driven incentives found in traditional brokerage firms. True RIAs are different.

In the best version of the RIA model, the client hires the advisor directly, and the advisor has the freedom to select the custodians, investment managers, planning tools, and solutions that best fit the client’s needs. The advisor acts as an architect rather than a salesperson for a parent company’s platform. Instead of asking, “What can I offer from my firm’s shelf?” the advisor can ask, “What is the best solution available for this client?”

The difference is not that RIAs have better people. The difference is that RIAs have a better structure.

Good advisors exist throughout the industry. There are exceptional advisors at large institutions and mediocre independent firms. Structure alone does not guarantee competence, ethics, or wisdom. But structure does influence behavior. It shapes incentives, decision-making, and ultimately the client experience.

In my view, the RIA model creates better alignment because it places the client at the center of the relationship. It gives good advisors greater flexibility, greater objectivity, and greater freedom to act in the client’s best interest. It also tends to attract entrepreneurial advisors who want to build customized solutions and long-term relationships rather than fit clients into a larger corporate system.

At the end of the day, investors are not simply choosing a person. They are choosing a structure and an incentive system. They are choosing where the arrows inside the triangle point.

The most important question is not how large the firm is, how impressive the marketing brochure looks, or even what products are being recommended. It is understanding who the advisor ultimately works for when interests are not perfectly aligned.

In my view, the strongest wealth management relationships are built when the client, not the institution, is in charge.